![]()

RISK AVERSION: A preference for risk in which a person prefers guaranteed or certain income over risky income. Risk aversion arises due to decreasing marginal utility of income. A risk averse person prefers to avoid risk and is willing to pay to do so, often through the purchase of insurance. This is one of three risk preferences. The other two are risk neutrality and risk loving.Risk aversion is one of three alternative preferences for risk based on the marginal utility of income. A risk averse person has decreasing marginal utility of income. With decreasing marginal utility of income a risk averse person obtains more utility from certain income than an equal amount of income involving risk. With risk, the utility from winning is exceeded by the utility from losing. Even though the expected income is equal to the certain income, the utility obtained from the certain income exceeds the utility obtained from the expected income. A risk averse person is better off avoiding risk. Because a risk averse person obtains more utility from certain income than from risky income, it follows that a smaller amount of certain income generates the same utility as the risky income. This means that a risk averse person is actually willing to pay to avoid risk. This difference in income is termed the risk premium and is the maximum price that a risk averse person would pay for an insurance policy that eliminates the risk. Two other risk preferences are risk loving and risk neutrality. A risk loving person has increasing marginal utility of income and prefers risky income to certain income. A risk neutral person has constant marginal utility of income and prefers risky income and certain income equally. Marginal Utility of Income

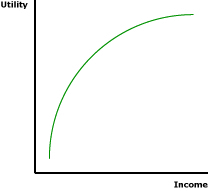

The standard view in consumer demand theory is that the marginal utility of income decreases with an increase in the quantity consumed. This gives justification for the negatively-sloped demand curve. This view also generally applies to the marginal utility of income. An increase in income results in a decrease in marginal utility. Decreasing marginal utility of income results in risk aversion. However, the marginal utility of income can also increase, leading to risk loving. Or the marginal utility of income can remain constant, leading to risk neutrality. The exhibit to the right presents decreasing marginal utility of income. At low levels of income, the curve is relatively steep, then grows flatter at higher income levels. A curve of this shape is commonly termed concave. It indicates that the change in marginal utility begins relatively high, then decreases as income increases. Decreasing marginal utility of income, represented by a concave curve, is the key to risk aversion. Increasing and constant marginal utility of income, represented by a convex curve and a straight line, give rise to risk loving and risk neutrality, respectively. Risk or Certainty?Risk aversion is revealed by different preferences for income obtained with certainty and an equal amount of income that involves risk. Consider these two related concepts:

The $100 that Pollyanna has at the start, and would keep if she did not wager, is the certain income. If she wants to keep this $100, then she can walk away from the wager. The risky income is the amount of income that she can expect to have after the wager. It's not $50 or $150, but the average of the two, $100, weighted by the probability of winning or losing. In other words, the expected income of a 50-50 wager is the amount of income she would expect to end up with after undertaking the wager a number of times, say a 100 or more. If she undertakes this wager 100 times, she can expect to win $50 exactly half of the time and lose $50 exactly half of the time. The loses exactly balance the wins and the income she can expect to end up with is $100. This can be summarized with the following equation. Expected income is the income generated by a loss, weighted by the probability of losing (p), plus the income generated by a win, weighted by the probability of win (1-p). The expression in the first set of brackets is the income from losing [(0.5) x $50]. The expression in the second set of brackets is the income from winning [(0.5) x $150]. The sum of the two expressions is the income expected from the wager, the average income obtained resulting after many wagers. The Utility of IncomeWhile income is obviously important, risk aversion is based on the utility generated by the income. This is where decreasing marginal utility of income plays a key role. Two related utility concepts are worth noting. One is the utility of expected (or certain) income and the other is expected utility.

In contrast, expected utility is identified by separately calculating the income from a loss, and the corresponding and the income from a win, then determining the utility from each. These utility values are then averaged, weighted by the probability of a loss and a win.

Working Through a Graph

Let's re-evaluate the $50 flip-of-a-coin wager facing Pollyanna Pumpernickel.

However, another important implication can also be had, the risk premium. This is the amount that Pollyanna would be willing to pay to avoid the risk. It can be identified by noting the amount of income that would generate the same utility as the expected utility of the wager. A click of the [Risk Premium] button reveals this information. Note that $82 of income generates the same utility, U(82), as the expected utility from the wager EU(100). The difference between these two income levels $100 and $82, is the risk premium. That is, Pollyanna is willing to pay up to $25 to avoid the wager, to avoid the risk. This is the price she would be willing to pay for an insurance policy that eliminates this risk. Other Risk PreferencesRisk aversion is one of three risk preferences. The other two are risk loving and risk neutrality.

Check Out These Related Terms... | risk preferences | risk neutrality | risk loving | marginal utility of income | risk | uncertainty | risk pooling | risk premium | economics of uncertainty | Or For A Little Background... | economics | microeconomics | market | scarcity | efficiency | sixth rule of ignorance | marginal utility | demand curve | paper economy | consumer demand theory | And For Further Study... | public choice | economics of information | innovation | good types | market failures | financial markets | institutions | insurance | information | efficient information search | information search | asymmetric information | adverse selection | moral hazard | signalling | screening | rational ignorance | market failures | Recommended Citation: RISK AVERSION, AmosWEB Encyclonomic WEB*pedia, http://www.AmosWEB.com, AmosWEB LLC, 2000-2025. [Accessed: December 17, 2025]. |

![]()